One of many many issues it’s important to determine while you begin a brand new job is the brand new firm 401(ok).

Consider it or not, we’ve got plenty of purchasers beginning new jobs these days. Sure, even amidst all of the tech-industry gloom and nervousness, new (and good!) jobs are available. And it seems that one of the crucial complicated components of getting a brand new job—and subsequently a brand new 401(ok)—mid-year is, “How a lot ought to I contribute to my new 401(ok)?”

That is one thing that our purchasers ask us about on a regular basis, so allow us to share with you what we share with them.

Why This Is Arduous to Determine Out

The problem is that, even if you happen to work at two firms and take part in each their 401(ok)s throughout a single calendar 12 months, you’re restricted to a contribution of $22,500 to a pre-tax or Roth account throughout each these 401(ok)s.

($22,500 is the restrict for 2023. It was $20,500 in 2022. And it’ll be even larger subsequent 12 months.)

In the event you didn’t contribute to your previous job’s 401(ok), then don’t fear about it! You may have the complete $22,500 at your disposal within the new job’s 401(ok).

However if you happen to contributed some cash to your previous job’s 401(ok), it’s important to contribute that a lot much less to your new job’s 401(ok). It’s not multivariable calculus (that I really discovered enjoyable), however it will probably get complicated.

Ah, the Irony

At Move, we use Guideline as our 401(ok) administrator. As a result of we use Guideline, our tiny, three-person agency will get entry to a very great tool that a lot of the Huge Boys (ex., Constancy) don’t supply:

Their web site supplies a instrument that shortly and simply tells you the way a lot you must contribute per paycheck as a way to max out your 401(ok) by the top of the 12 months. The instrument works whether or not you’ve contributed to a different 401(ok) earlier within the 12 months or are ranging from scratch.

Surprisingly, Constancy and all the opposite 401(ok) plan suppliers that our purchasers’ big tech employers use don’t, so far as we will inform, supply something like this.

Which is why we’ve got our personal ugly, in-house Google Sheets calculator for our purchasers.

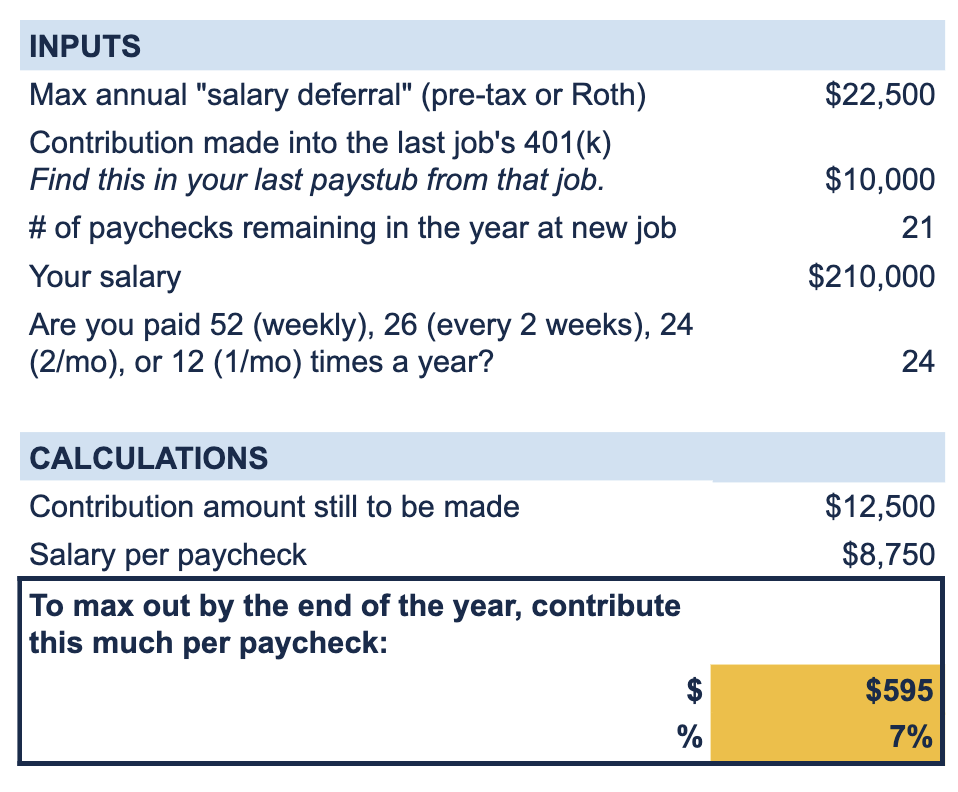

Calculating How A lot to Contribute Per Paycheck

You possibly can see our calculator, and make a duplicate if you would like. (I don’t have full confidence that sharing the calculator this fashion will work. If it doesn’t, then attain out and we’ll ship it to you.)

(I had initially written, “… although I think about the web is awash in comparable calculators.” However then I really regarded and didn’t see any such calculators on the primary web page of outcomes. There are heaps of 401(ok) contribution calculators, however all of them appear to be of the kind “inform us how a lot you save to your 401(ok) and we’ll let you know what number of {dollars} you’ll have while you retire” or vice-versa.)

Right here’s the non-interactive model of it:

What Does the Calculator Do?

- It figures out how way more cash you’re allowed to contribute to your new 401(ok) for the remainder of the 12 months, primarily based on how a lot cash you contributed to your final 401(ok).

- It then calculates what number of {dollars} (or proportion of earnings) you need to contribute to your new 401(ok) per paycheck, primarily based on what number of paychecks you’ve got remaining within the 12 months and the pre-tax measurement of every paycheck, as a way to attain that $22,500 max by 12 months’s finish.

To make use of the calculator, you must enter a number of items of information that may be deceptively exhausting to determine.

- Contribution made into the final job’s 401(ok): You gotta understand how a lot you set into your earlier firm’s 401(ok).

It’s best to be capable of determine this out by wanting on the final paystub from that job. There ought to be a line merchandise in your 401(ok) (possibly two, if you happen to put cash into each the pre-tax and Roth accounts), and a “YTD” (12 months thus far) quantity for it. That’s how a lot you contributed this whole 12 months to this point into that 401(ok).

Right here’s part of a shopper’s precise paystub. I’ve “circled” the year-to-date contributions into the 401(ok) pre-tax and Roth. This paystub even has a 3rd contribution line merchandise: contribution from a bonus!

This shopper has to date contributed $5,979.16 to their 401(ok) and subsequently can contribute one other $22,500 – $5979.16 = $16,530.84. (Pricey God, let my arithmetic be proper.)

- # of paychecks remaining within the 12 months at new job and Are you paid 52 (weekly), 26 (each 2 weeks), 24 (2/mo), or 12 (1/mo) occasions a 12 months?: That is kinda tough. It’s important to know the frequency with which you receives a commission, which hopefully you do, or will quickly after beginning the brand new job.

Most probably you receives a commission both each two weeks (26 occasions/12 months) or twice per thirty days (24 occasions/12 months). For instance, if you happen to receives a commission twice per thirty days and begin contributing to your new 401(ok) on August 1, then you’ve got 5 months and subsequently 10 paychecks remaining.

{kind=link}

- Your wage: You’d be shocked how many individuals don’t know their salaries, however hopefully if you happen to’re simply beginning a brand new job, that supply letter continues to be contemporary in your thoughts.

Random Notes

When you begin digging, 401(ok)s supply up boundless complexity. Right here’s a smattering of associated tidbits to remember:

- Let’s say you contribute extra to this new 401(ok) than you need to, and your whole contribution throughout each 401(ok)s is over $22,500. It’s not the top of the world. You will must take away the “extra” contributions after the top of the 12 months, which you’ll discover out not less than while you do your taxes.

This may be an administrative problem, so ‘tis higher to not run afoul of this. Any mistake on this planet of monetary forms can simply flip right into a nightmare for no rattling good cause.

- We now have had some purchasers who had an employer/HR division that helped them determine the remaining 401(ok) contribution. In the event you’re fortunate sufficient to work at such an organization, nice! No must do your individual calculations. Understanding what’s taking place would nonetheless be good, although.

- We’ve been speaking about this $22,500 cap. Technically, your actual 401(ok) contribution cap is $66,000 (in 2023), not $22,500. That further $43,500 might be put into your 401(ok) by your employer (mostly by the use of a match) or by you, in case your 401(ok) plan permits after-tax contributions.

Apparently sufficient, if in case you have a couple of 401(ok) in the middle of one 12 months, you’ll be able to contribute that $22,500 solely as soon as throughout all of your 401(ok)s, however you’ll be able to contribute as much as the $66k restrict in each single 401(ok).

In sensible phrases, this in all probability isn’t all that helpful. You’d need to have two (or extra) 401(ok)s, every allowing after-tax 401(ok) contributions, you’d max out $22,500 solely as soon as, after which contribute as much as $66k in every of your 401(ok)s. (This example is finicky and there are many guidelines, so I’m solely giving a obscure nod to the probabilities right here.)

- In the event you’re 50 years previous or older, that $22,500 is as an alternative $30,000 and that $66,000 is as an alternative $73,500.

- I like to recommend setting a calendar reminder for your self close to the top of the 12 months, when you’ve got a few paychecks left. At the moment, I like to recommend how a lot you’ve contributed to each your 401(ok)s to date that 12 months, and make changes (up or down!) if you happen to’re not going to hit that $22,500 max within the final paycheck of the 12 months.

If you begin a brand new job, you’ve received a ton of issues to determine, most essential of which is your precise job. Fortunately, you would possibly be capable of moderately wait a couple of paychecks to essentially determine your new 401(ok).

Oh, and congratulations on the brand new job!

Do you need to work with a monetary planner who may also help you determine irritating, nitty-gritty particulars? Attain out and schedule a free session or ship us an e-mail.

Join Move’s twice-monthly weblog e-mail to remain on high of our weblog posts and movies.

Disclaimer: This text is supplied for instructional, basic data, and illustration functions solely. Nothing contained within the materials constitutes tax recommendation, a advice for buy or sale of any safety, or funding advisory providers. We encourage you to seek the advice of a monetary planner, accountant, and/or authorized counsel for recommendation particular to your scenario. Replica of this materials is prohibited with out written permission from Move Monetary Planning, LLC, and all rights are reserved. Learn the complete Disclaimer.