{kind=link}

For the reason that international monetary disaster, the Federal Reserve has relied on two foremost charges to implement financial coverage—the speed paid on reserve balances (IORB charge) and the speed supplied on the in a single day reverse repo facility (ON RRP charge). On this put up, we discover how these instruments steer the federal funds charge throughout the Federal Reserve’s goal vary and the way efficient they’ve been at supporting charge management.

The Federal Reserve’s Financial Coverage Implementation Framework

The Federal Open Market Committee (FOMC) communicates its stance of financial coverage by a goal vary for the federal funds (fed funds) charge—the rate of interest at which banks borrow funds in a single day on an unsecured foundation within the fed funds market. The Federal Reserve (the Fed) at present implements financial coverage in a regime of ample reserves, the place management over the fed funds and different short-term rates of interest is exerted by two administered charges set by the Fed: the IORB charge and the ON RRP charge.

The IORB is the speed that the Fed pays on the reserves that banks maintain in a single day of their Fed accounts, thereby setting a flooring on the charges at which banks lend in a single day within the fed funds market. The Fed has paid IORB since October 2008. Banks, nevertheless, are solely liable for a fraction of the lending exercise within the fed funds market and different U.S. cash markets. For that reason, the Fed employs a second lever: the ON RRP charge. The ON RRP facility permits eligible establishments, together with cash market funds, government-sponsored enterprises, and first sellers, to speculate in a single day with the Fed on the ON RRP charge. This second lever, which was added to the Fed coverage toolkit in 2014, works equally to the IORB charge, establishing a flooring on the charges at which these non-bank establishments are keen to lend funds in a single day.

Adjustments within the Goal Vary and the Fed Funds Price

When the FOMC pronounces a change within the goal vary for the fed funds charge, it implements this transformation by changes within the administered charges. However how a lot of the change passes by to the charges within the fed funds market?

To reply this query, we have a look at all FOMC conferences between December 2015 and June 2023 by which both the goal vary or the administered charges (IORB and/or ON RRP) have been modified. There are twenty-seven such conferences. For the reason that width of the goal vary has remained fixed, our outcomes are the identical whether or not we have a look at the highest or backside of the vary. We use an occasion examine methodology and examine the rates of interest on fed funds transactions earlier than and after the FOMC bulletins.

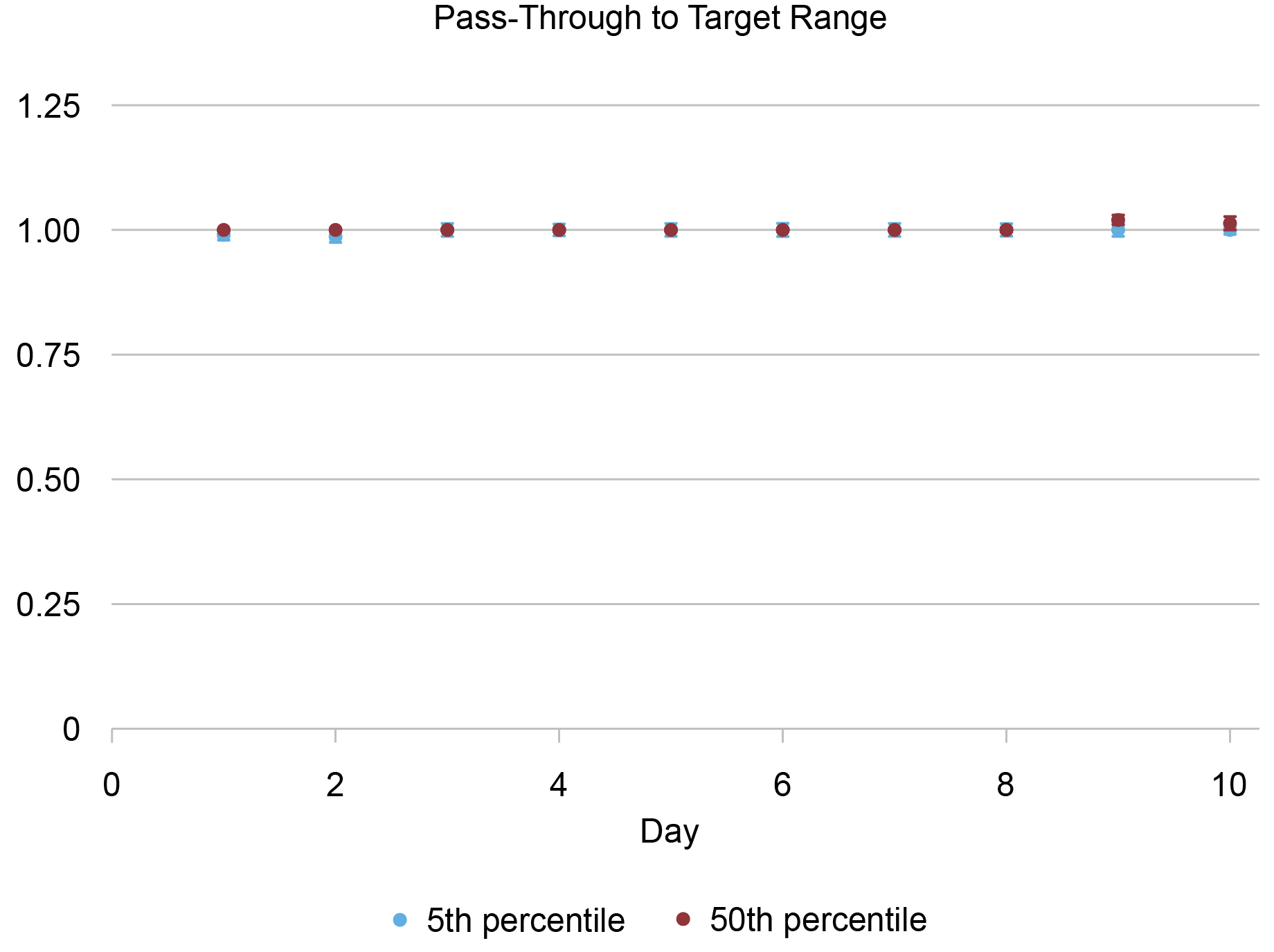

The chart beneath summarizes the outcomes of a sequence of transaction-level quantile regressions estimating how the median (crimson) and the fifth percentile (blue) of the distribution of fed funds charges responded to a change within the goal vary. The coefficients on day 1 examine the charges prevailing someday earlier than and someday after the assembly, on day 2, two days earlier than and after the assembly, and so forth, all the best way to 10 days earlier than and after the assembly on day 10.

Adjustments within the Goal Vary Cross By One-to-One to Fed Funds Charges

Sources: FR 2420, Report of Chosen Cash Market Charges, Federal Reserve Financial Knowledge (FRED); authors’ calculations.

Notice: Goal vary represents the Federal Open Market Committee goal vary for the federal funds charge.

Forever-windows, the response of the median fed funds charge to adjustments within the goal vary could be very near 1—that’s, a 1 foundation level improve within the goal vary strikes the median fed funds charge by the identical quantity. The response could be very comparable for the left tail of the distribution (that’s, for the fifth percentile). Along with a pass-through near 1, the impact is current on the primary day after the FOMC communicates the change in coverage stance.

Technical Changes

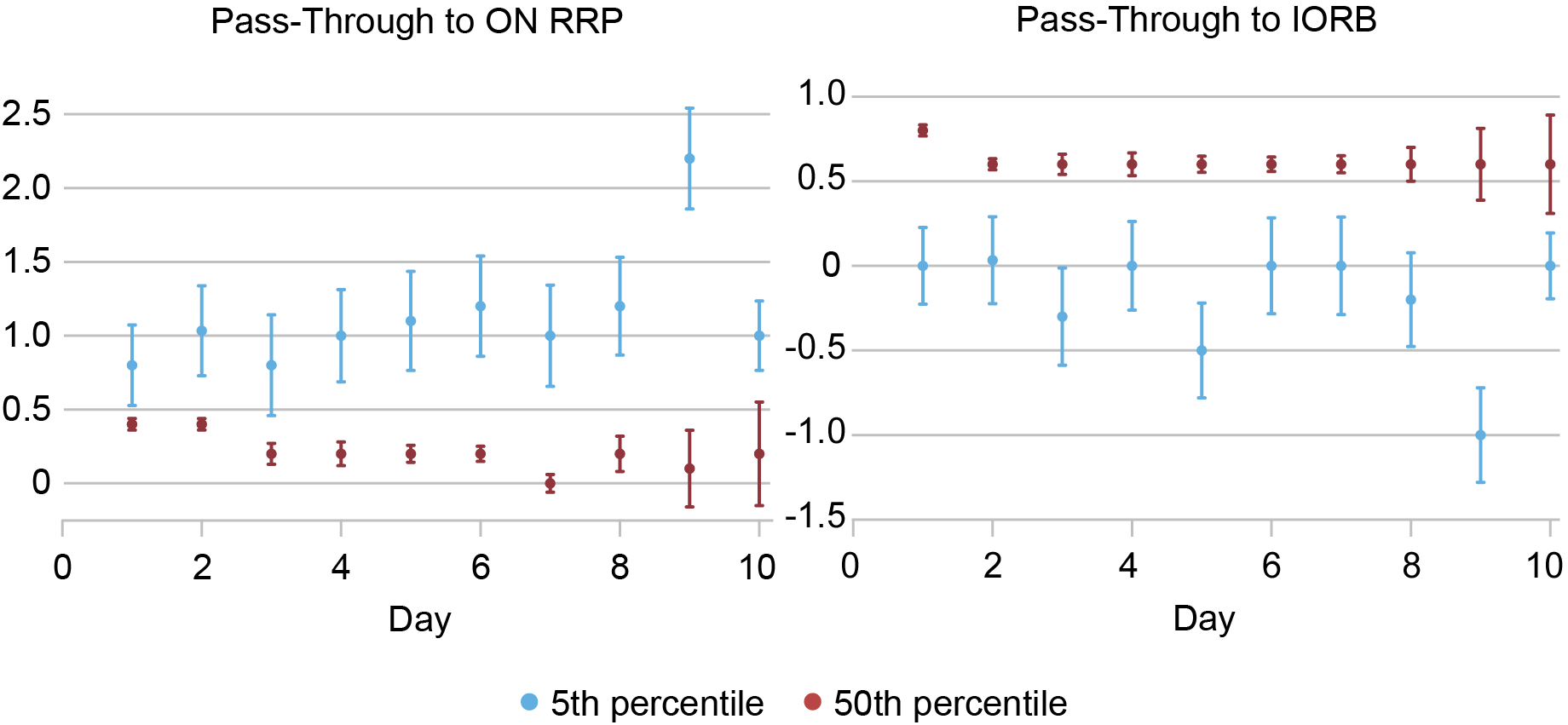

In most FOMC conferences, the IORB and ON RRP charges are adjusted by the identical quantity because the goal vary. Nevertheless, in seven of the twenty-seven FOMC conferences in our pattern, both the IORB or the ON RRP charge have been adjusted by a special quantity than the goal vary, a so-called technical adjustment. As an example, on Could 2, 2019, the IORB charge was modified from 2.4 p.c to 2.35 p.c, whereas the goal vary and ON RRP charge have been left unchanged. Due to this, we will estimate the influence of adjusting the extent of those administered charges with respect to that of the goal vary.

The left panel of the chart beneath exhibits the estimated influence of adjustments within the ON RRP charge with respect to the goal vary on the median (crimson) and fifth percentile (blue) of the distribution of fed funds charges. The suitable panel presents comparable estimates for changes within the IORB charge relative to the goal vary.

ON RRP and IORB Charges Cross By to Fed Funds Charges Otherwise

Sources: FR 2420, Report of Chosen Cash Market Charges, Federal Reserve Financial Knowledge (FRED); authors’ calculations.

Notes: ON RRP is the in a single day reverse repo charge. IORB is the curiosity on reserve balances charge.

Adjusting the IORB and ON RRP charges with respect to the goal vary impacts the distribution of charges on fed funds transactions otherwise. A change within the IORB charge relative to the goal vary primarily impacts the median of the distribution, shifting it up or down by extra if the IORB adjustments greater than the vary and by much less in any other case.

In distinction, adjustments within the charge supplied on the ON RRP facility with respect to the goal vary have a smaller influence on the median fed funds transaction whereas resulting in a pass-through near 1 for the fifth percentile—the left tail of the distribution. That is, certainly, per the aim of the ON RRP facility: firming the ground for transactions within the fed funds market.

Summing Up

The Fed depends on the IORB and ON RRP charges to implement financial coverage. These two administered charges have proven to be very efficient at sustaining the fed funds charge throughout the goal vary. Whereas they work by comparable channels—steering the charges at which cash market members are keen to lend funds in a single day—they affect the distribution of fed funds charges otherwise, with the IORB charge primarily affecting the median and the ON RRP charge the left tail.

Gara Afonso is the top of Banking Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Marco Cipriani is the top of Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Gabriele La Spada is a monetary analysis economist in Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

On the time this put up was written, Peter Prastakos was a senior analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The way to cite this put up:

Gara Afonso, Marco Cipriani, Gabriele La Spada, and Peter Prastakos, “The Federal Reserve’s Two Key Charges: Comparable however Not the Identical?,” Federal Reserve Financial institution of New York Liberty Road Economics, August 14, 2023, https://libertystreeteconomics.newyorkfed.org/2023/08/the-federal-reserves-two-key-rates-similar-but-not-the-same/.

Disclaimer

The views expressed on this put up are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).