{kind=link}

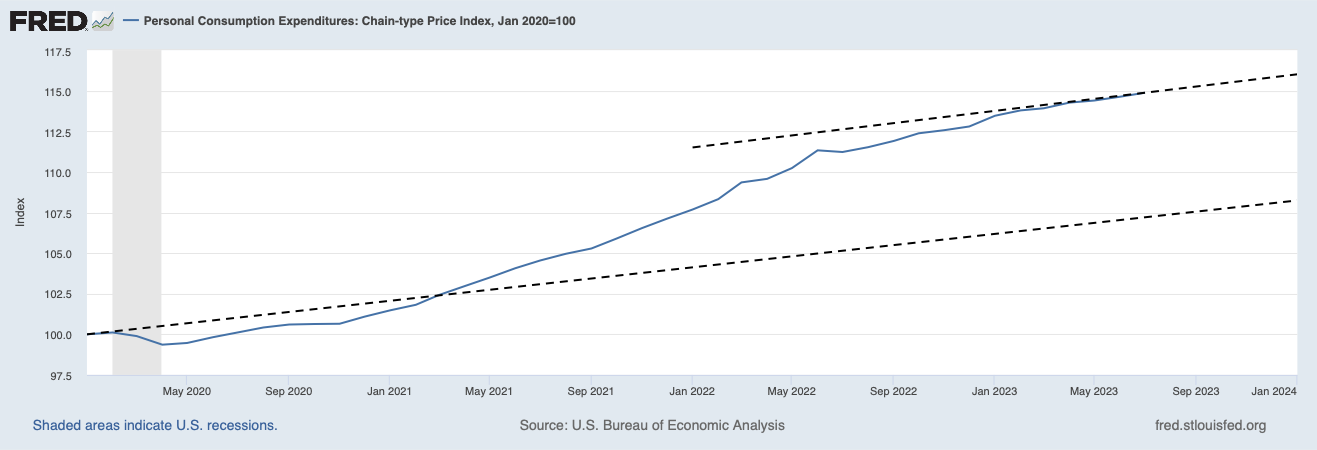

After greater than two years of excessive inflation, the Federal Reserve lastly has inflation again on track. The Private Consumption Expenditures Worth Index (PCEPI) has grown at a constantly compounding annual fee of two.1 p.c during the last three months, new information from the Bureau of Financial Evaluation exhibits. Bond markets are pricing in roughly 2 p.c PCEPI inflation per yr over the subsequent 5 years.

Some—together with some Fed officers—are reluctant to just accept the excellent news. And their reluctance is comprehensible. Annual inflation charges stay excessive. The PCEPI grew 4.0 p.c during the last yr. Core PCEPI, which excludes unstable meals and vitality costs, grew 4.2 p.c. Nevertheless, these excessive charges largely mirror value will increase that occurred months in the past. These distant value will increase shouldn’t be used to justify additional fee hikes as we speak.

An analogy serves as an example. Suppose you decelerate from 45 MPH to twenty MPH whereas approaching a college zone in your automotive. If you attain the varsity zone, you look down at your odometer and see that you’re going 20 MPH. At that time, you don’t stomp on the brake simply because you’ve gotten averaged 35 MPH during the last quarter mile. After all your common during the last quarter mile is bigger than your 20 MPH goal: you have been decelerating to hit that concentrate on. What issues now will not be how briskly you have been going, however how briskly you are going.

Likewise, the Fed is aiming for two p.c inflation. Now, inflation is again round 2 p.c. The Fed shouldn’t increase charges additional simply because inflation was increased months in the past. What issues now will not be how briskly costs have been rising, however how briskly they are rising now.

After all, the worth degree stays a lot increased than it will have been had the Fed hit its 2-percent goal over the course of the pandemic. If inflation had averaged 2 p.c, they’d be 7.7 share factors decrease as we speak. However that, too, will not be a very good motive for elevating charges additional.

On the whole, the Fed ought to set expectations after which ship on these expectations. The primary-best coverage is obvious: when a change in nominal spending pushes the worth degree above (beneath) the projected path, the Fed ought to promptly tighten (loosen) coverage to convey these costs again in keeping with expectations. The Fed has not completed this. Nevertheless it doesn’t comply with that the Fed ought to do that now. For the reason that Fed didn’t act promptly, the first-best possibility is off the desk. We are able to solely hope for a second-best coverage. We should significantly take into account what the Fed ought to do when it hasn’t completed what it ought to have completed.

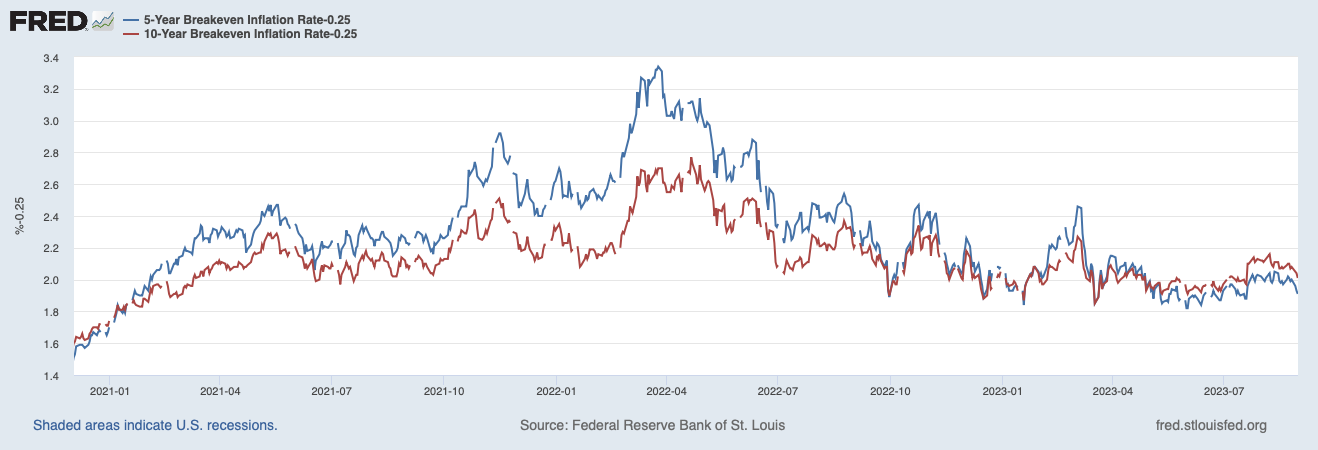

On condition that the Fed has made it clear—since at the very least December 2021—that it will step by step convey the speed of inflation again right down to 2 p.c however allow the worth degree to stay elevated, it will be a mistake to alter course now and attempt to convey costs again right down to the place they’d have been had it by no means erred within the first place. Folks have adjusted their expectations. As proven beneath, the TIPS unfold—adjusted for the distinction between PCEPI inflation and Shopper Worth Index Inflation—suggests market members are pricing in 1.9 p.c inflation over the five-year horizon and a pair of.0 p.c inflation over the ten-year horizon.

Extra importantly, folks have renegotiated their wages and buy orders with these new expectations in thoughts. To course right at this late stage would quantity to a really painful contraction.

We’ve already borne the prices of an sudden inflation. There’s no good motive to tack on extra prices from an sudden deflation.

William J. Luther

William J. Luther is the Director of AIER’s Sound Cash Challenge and an Affiliate Professor of Economics at Florida Atlantic College. His analysis focuses totally on questions of foreign money acceptance. He has printed articles in main scholarly journals, together with Journal of Financial Habits & Group, Financial Inquiry, Journal of Institutional Economics, Public Alternative, and Quarterly Evaluate of Economics and Finance. His standard writings have appeared in The Economist, Forbes, and U.S. Information & World Report. His work has been featured by main media shops, together with NPR, Wall Avenue Journal, The Guardian, TIME Journal, Nationwide Evaluate, Fox Nation, and VICE Information. Luther earned his M.A. and Ph.D. in Economics at George Mason College and his B.A. in Economics at Capital College. He was an AIER Summer time Fellowship Program participant in 2010 and 2011.