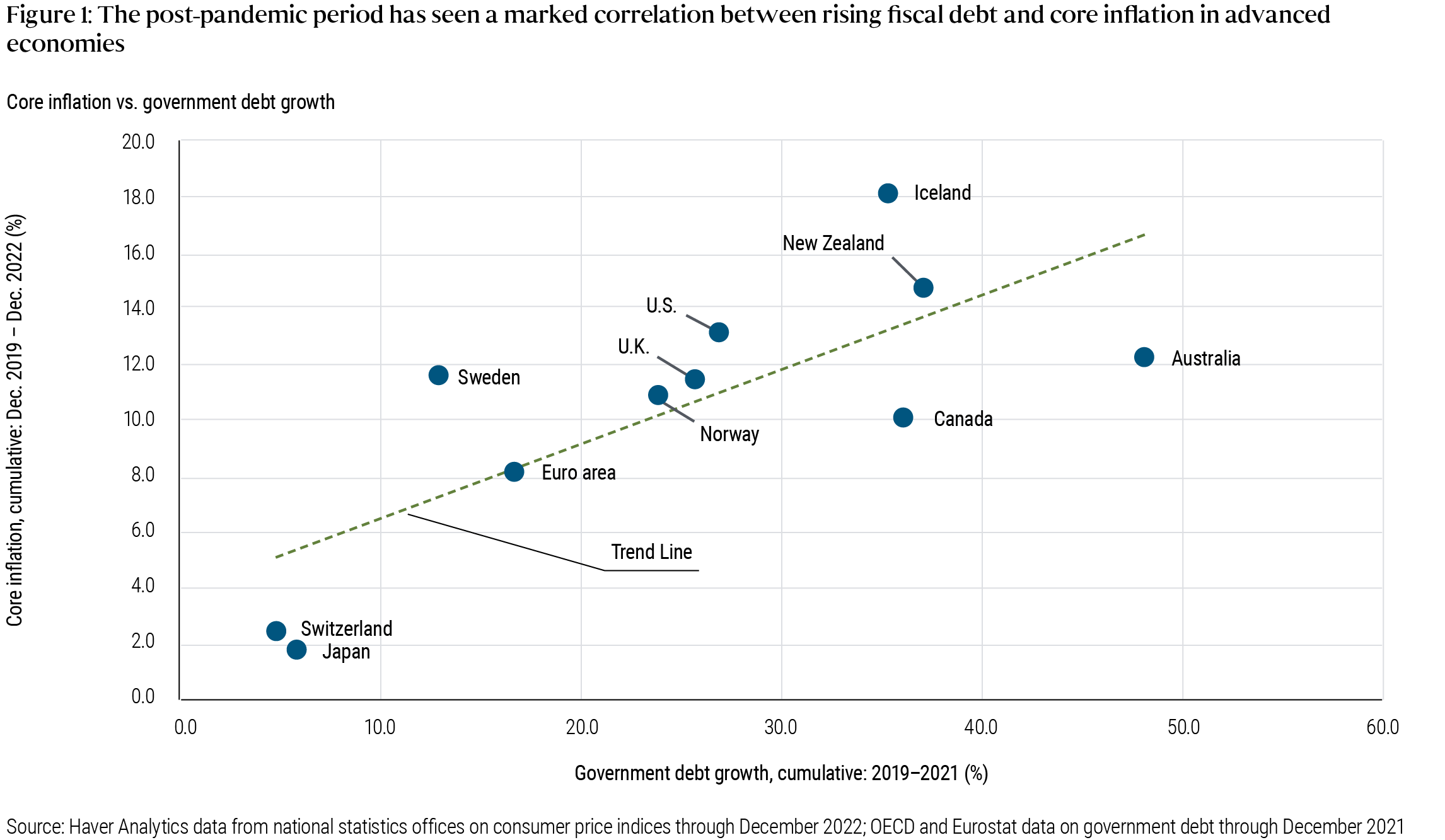

Peder Beck-Friis and Richard Clarida at Pimco have a pleasant weblog publish on the latest inflation, together with the above graph. I’ve puzzled, and been requested, if the variations throughout international locations in inflation strains up with the dimensions of the covid fiscal enlargement. Apparently sure.

It is a easy truth, and it is harmful to crow too loudly when issues go your means. Fiscal concept says that inflation comes when debt or deficits exceed expectations of a rustic’s potential or will to repay. The latter can differ rather a lot. So, it doesn’t predict a easy relationship between debt or deficits and inflation. Nonetheless, it is good when issues come out that means, and extra enjoyable to put in writing {qualifications} than to give you excuses for a opposite consequence!

I’ve seen different proof that does not look so good (will publish when it is public). One instance is throughout eurozone international locations. However that is a superb reminder the place to count on success and the place to not count on success. Inflation as described by most macro fashions, together with fiscal concept, monetarism, and many others., is the element widespread to all costs and wages. It’s in essence the autumn within the worth of foreign money. In any historic expertise we see a number of relative value adjustments on prime of that, particularly costs over wages. Certainly inflation is just measured with costs, and a central thought is to measure the “price of dwelling,” not the worth of the foreign money. Throughout the eurozone there is just one foreign money and thus just one underlying inflation. The massive variation in measured inflations are relative costs, actual alternate charges between international locations, and may’t go on endlessly. That we can not hope to clarify inflation variation throughout international locations within the eurozone with a easy concept that describes the worth of foreign money provides you some sense of the error bars on this train as effectively.

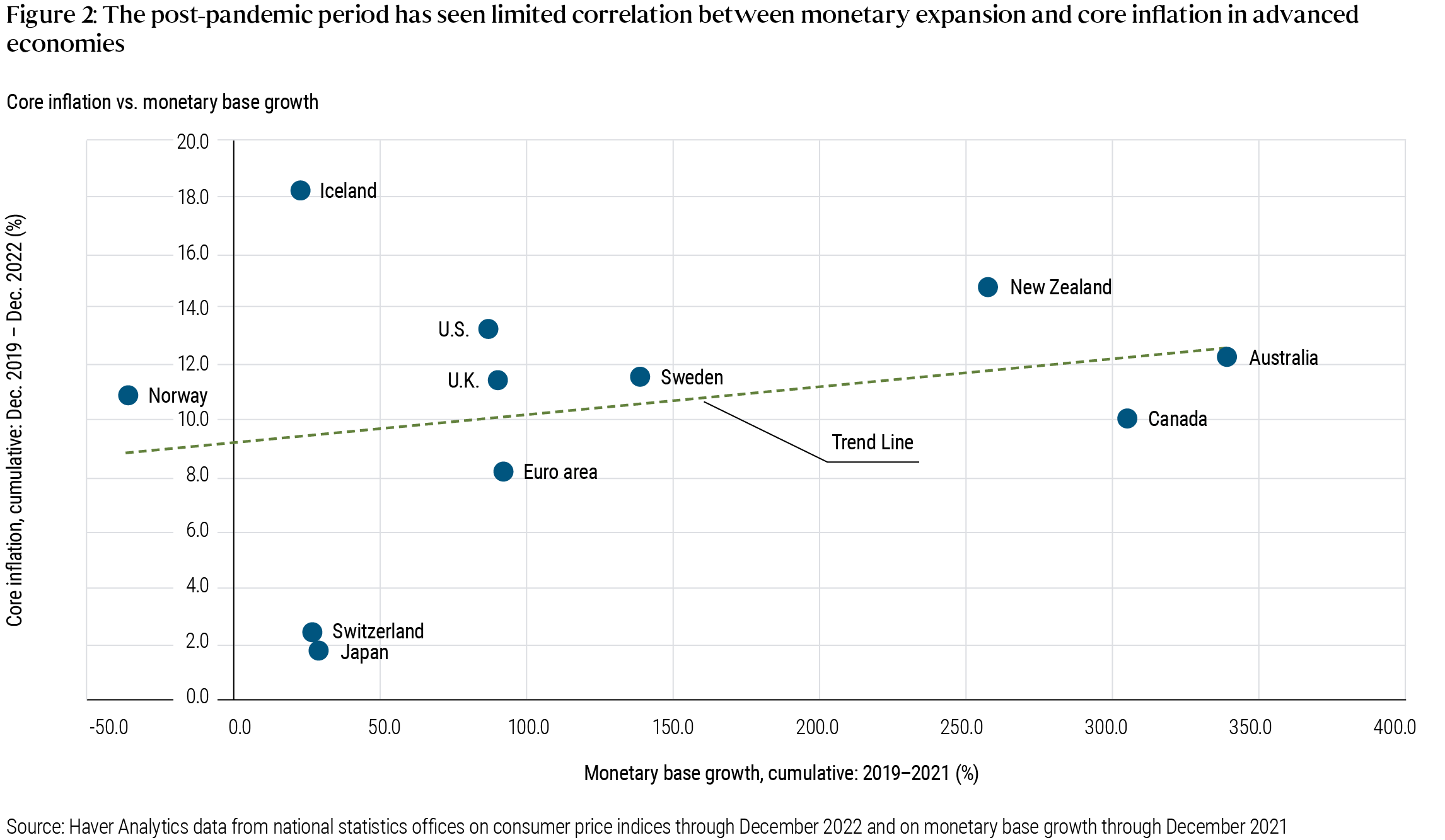

Beck-Friis and Clarida additionally have a look at cash development, above. There was an enormous enlargement in M2 earlier than the US inflation. Monetarists took a victory lap. M2 has since fallen rather a lot. There may be not a lot correlation between financial enlargement and inflation throughout international locations nonetheless. The slope of the regression additionally clearly depends upon one or two factors.

Cash or debt, which is it? When governments print cash to finance deficits (or interest-bearing reserves), fiscal concept and financial concept agree, there’s inflation. Printing cash (helicopters) is probably notably highly effective, as debt carries a fame and custom of reimbursement, which cash could not carry. A core subject separating financial and monetary concept is whether or not an enormous financial enlargement with out deficits or different fiscal information would have any results. Would a $5 trillion QE (purchase bonds, subject cash) with no deficit have had the identical inflationary affect? Monetarists, sure; fiscalists, no.

Beck-Friis and Clarida opine that fiscal stimulus is over and central banks now have all of the levers they should management inflation. I am not so positive. The US continues to be working a trillion or so deficit regardless of a 3.6% unemployment price, and right here come entitlements. And, as weblog readers will know, I’m much less assured of the Fed’s lever. We will see.

Replace:

Mark Dijkstra makes the next graph (see feedback for hyperlink), based mostly on IMF knowledge for all international locations. Hmm, does not look so good.

Nonetheless, while you have a look at a number of small international locations, bizarre issues occur. The far proper knowledge level is Estonia, with 100% improve in debt and 14% cumulative inflation. Estonia began with 8.2% debt/GDP, nonetheless, so its rise to 18.4% is a 100% rise in debt to GDP ratio. So, Estonia spent 10% of GDP on covid and now army, in comparison with 30% of GDP for the US. Once more, fiscal concept shouldn’t be debt or deficit = inflation, however debt vs. potential and can to repay. One can argue that this improve in debt is extra repayable. Argentina has -8% development in debt/GDP and 100% inflation. Inflation is inflating away debt/GDP sooner than the federal government can print the debt. The excessive inflation international locations on this graph are Uzbekistan, Ghana, Guinea, Sierra Leone, Turkmenistan, Nigeria, Zambia, and Haiti. They’re all plausibly fiscal inflation, from preexisting fiscal issues, not steady international locations that all of the sudden borrowed/printed 30% of GDP with no plans to pay it again, the quite particular case of the US, EU, UK. OK, I am making excuses and I am glad I began with the cautionary paragraph. Fiscal concept shouldn’t be really easy as debt = inflation! However we do need to confront the numbers, and I hope this spurs some extra critical evaluation.