{kind=link}

A reader asks:

I’m anticipating needing to exchange each the roof on my home and a automobile 5 years from now. I want to have $100,000 put aside for these bills. 5 years out seems like an funding no man’s land. Shares appear to be a bit dangerous at the moment body, and excessive curiosity financial savings, whereas engaging now, will possible have charges dropped if the Fed drops rates of interest sooner or later. I’ve additionally thought-about doing one thing like a goal date fund by way of a robo advisor and having it handle the inventory and bond allocations, reducing danger over time. I plan to greenback value common all through the following 5 years as I’ve funds accessible to avoid wasting. Do you could have suggestions for the way to allocate financial savings given this timeframe? Are there different choices I ought to contemplate?

If we had been a lump sum the reply could be fairly easy proper now. Put your cash right into a 5 yr U.S. treasury bond yielding 4.5% or so and name it a day. That’s a fairly good return with an ideal asset-liability match for the longer term.

The truth that you’ll be saving cash periodically till you attain you purpose adjustments the equation a bit however we are able to nonetheless use that 5 yr time horizon to consider investing within the inventory marketplace for this type of intermediate-term purpose.

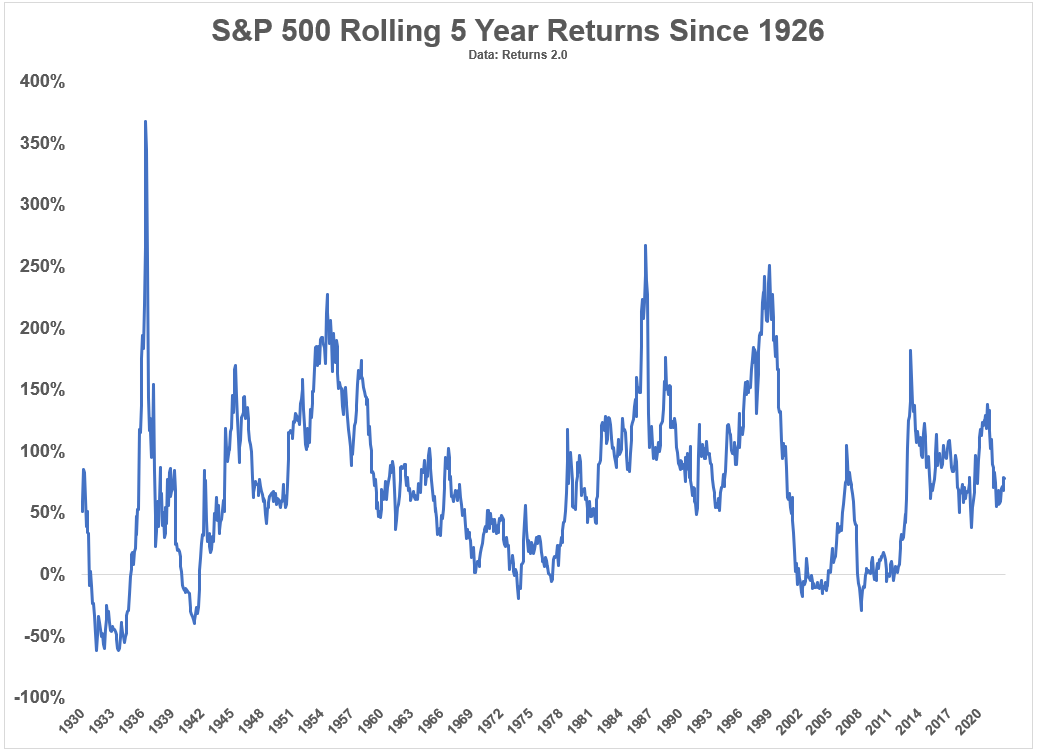

These are the rolling 5 yr complete returns for the S&P 500 going again to 1926:

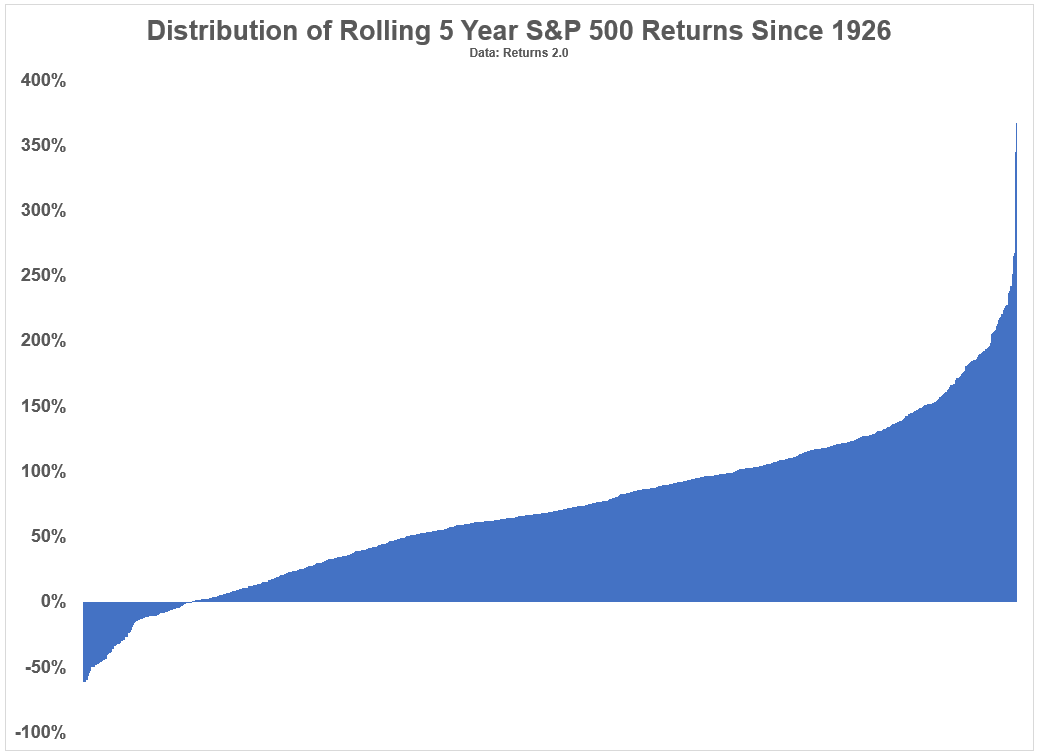

And right here’s one other means of these returns ranked from worst to greatest:

The excellent news is almost all of the time shares have been up on a 5 yr foundation. Returns had been constructive on 88% of all rolling 5 yr home windows.1

The unhealthy information is the vary of returns from greatest to worst has been fairly broad:

- Worst 5 yr return: -61%

- Greatest 5 yr return: +367%

To be truthful, each of those 5 yr home windows occurred within the Thirties however even when we have a look at post-WWII information, there may be nonetheless the potential for a variety of outcomes:

- Worst 5 yr return: -29%

- Greatest 5 yr return: +267%

I’ve a comparatively excessive tolerance for danger. But when I’m investing for a selected purpose sooner or later and I understand how a lot I’m going to wish and after I’m going to be spending the cash the inventory market is simply too dangerous for me until we’re speaking 5+ years or so.

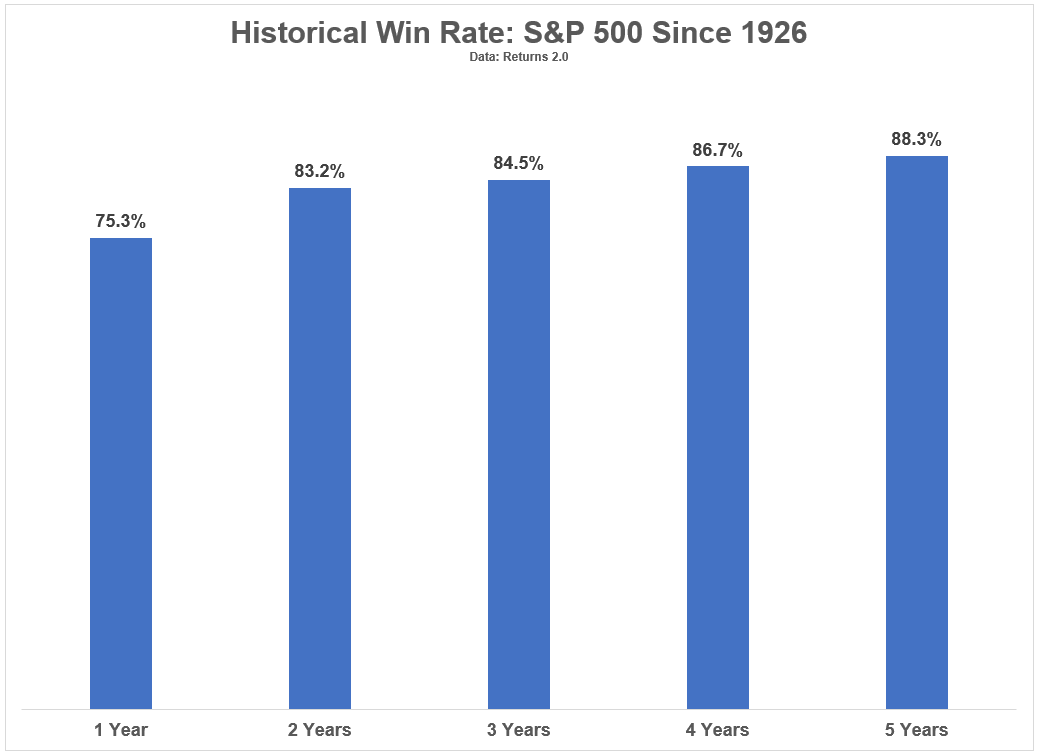

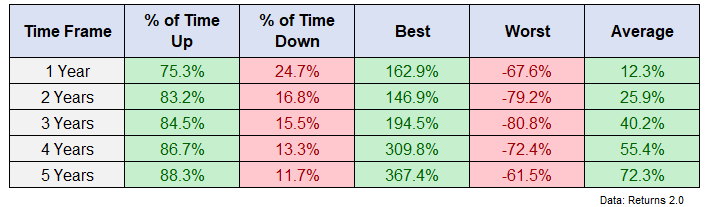

And because you’re going to be saving this cash over time as you method your finish date to spend on that new roof and automobile the inventory market goes to get even riskier. Listed here are the historic win charges over 1, 2, 3, 4 and 5 yr time horizons for U.S. shares:

The percentages are nonetheless in your favor however the vary of outcomes and the potential for loss will increase the shorter your time horizon goes:

Should you might simply financial institution on these common returns2 yr in and yr out you’d be set however the danger of seeing a loss on the actual second you want your money appears unappealing. It’s an pointless stage of economic stress so as to add to your life.

The concept of using a targetdate fund or robo-advisor makes extra sense than placing your whole cash into shares as a result of you could have the power to diversify and have some say over your danger tolerance and the timing of that purpose.

The Vanguard 2030 targetdate fund is presently 65% shares and 35% bonds. The 2025 fund is extra like 60/40.

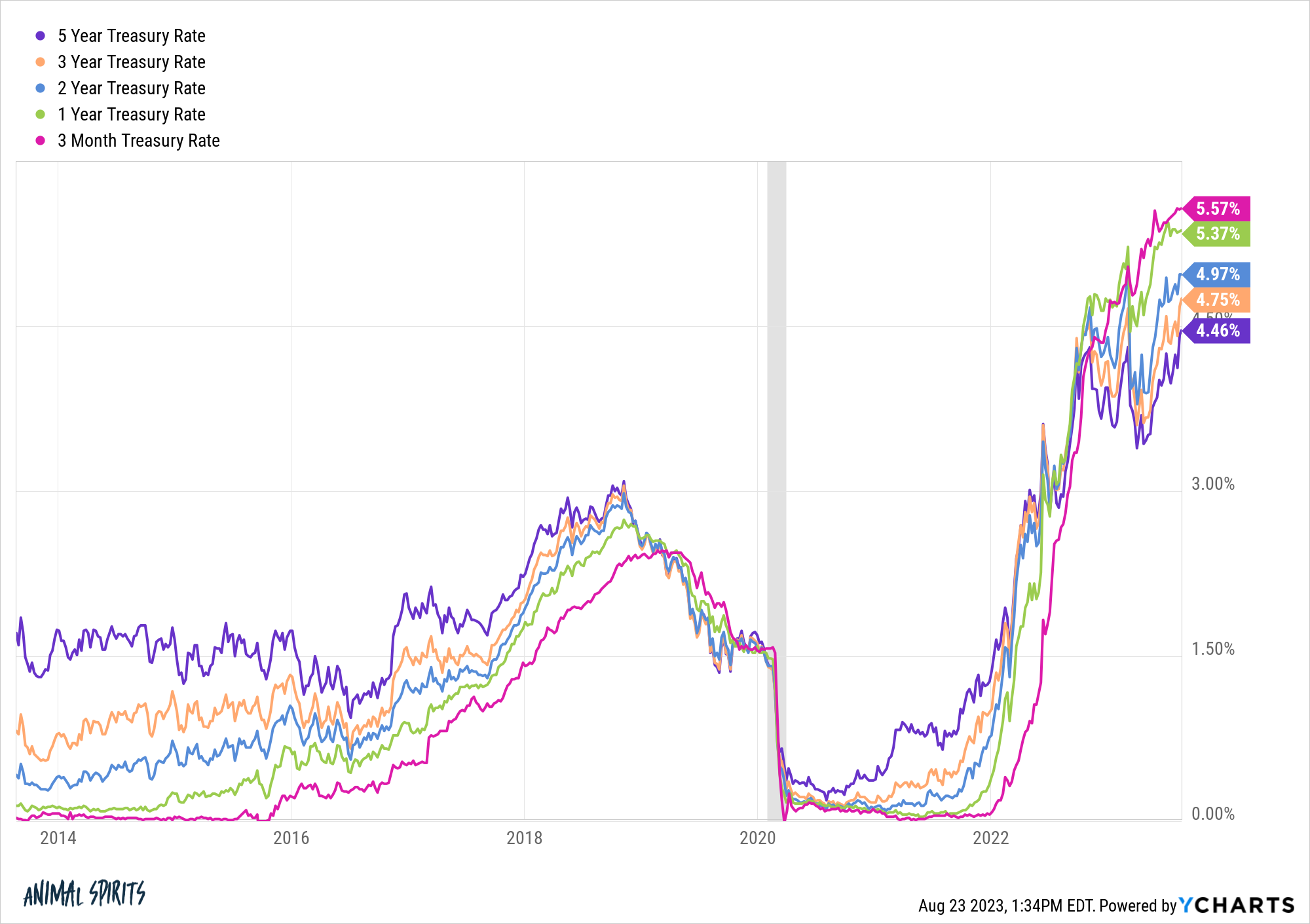

Some folks have a better urge for food for danger than I do on the subject of these items however I wouldn’t overcomplicate it if I had a purpose like this. Simply have a look at the charges you possibly can lock in on short-term Treasuries in the intervening time:

May charges fall once more? Certain. That’s a powerful chance within the coming years however you could have the power to lock in increased charges for longer now that the longer finish of the curve is catching up.

With regards to short-to-intermediate-term monetary targets I’ve 3 easy guidelines:

1. It needs to be liquid.

2. I’m not prepared to simply accept a lot volatility.

3. I don’t need the potential of massive losses after I must spend it.

You would earn more money by investing your financial savings in riskier securities. However the draw back of getting lower than you want when the invoice comes due far outweighs any extra beneficial properties you possibly can get by taking over extra danger.

We mentioned this query on the newest version of Ask the Compound:

Kevin Younger joined me on the present once more as we speak to speak about questions on early retirement, spending cash in your monetary targets, consolidating a number of HSAs and the way to pay for a renovation on your own home.

Additional Studying:

Rolling the Cube within the Inventory Market

1As common, I’m utilizing month-to-month complete returns (with dividends) for these efficiency numbers.

2I used easy arithmetic averages right here, not geometric for the quants scoring at house.