{kind=link}

As an investor you now have a plethora of funding choices accessible, starting from Mounted earnings securities like financial institution fastened deposits, bonds to Gold, Mutual Funds, Shares and to Cryptocurrencies.

Each funding you make has to undergo three completely different phases i.e.,

- Funding (or) Contribution stage

- Revenue Incomes Stage (or) Progress part

- Withdrawal or redemption or consumption part.

For instance: Let’s say you want to ebook a 5 12 months Financial institution Mounted Deposit for tax-saving function. The funding in FD is eligible for tax deduction underneath part 80c. That is within the funding part. Your capital earns ‘curiosity earnings’ for the subsequent 5 years. That is the earnings incomes part and its taxable on this case. Once you redeem the FD on maturity, the withdrawal quantity is tax-free (provided that tax is paid on the ‘progress or earnings incomes stage’ itself).

Tax Remedy of Saving & funding choices

Below every stage of the funding cycle, earnings can both be Taxed (T) or Exempted (E) from the taxes. So, we are able to have 6 doable mixtures of Es & Ts for 3 completely different phases as under;

- EEE : Exempt –> Exempt –> Exempt (which means you possibly can avail tax deductions on the time of funding, the earnings earned on this funding is tax exempted & even the maturity quantity is tax-free)

- EET : Exempt –> Exempt –> Tax

- ETE : Exempt –> Tax -> Exempt

- TEE : Tax –> Exempt – > Exempt

- TET : Tax –> Exempt -> Tax

- TTE : Tax –> Tax -> Exempt

Usually most of us have a tendency to select greatest investments based mostly on the tax therapy or the tax advantages accessible on the funding stage solely. Nevertheless, we’d like to concentrate on the taxation guidelines relevant in all of the three phases.

Persevering with with the above Tax-saving Financial institution FD – What sort of tax therapy does it belong to? Is it EEE or ETE?

The reply is, it belongs to the ETE (Exempt – Taxable – Exempt) tax regime. You get Tax-exemption (E) if you make investments, the curiosity earned on FD is taxable (T) and the maturity quantity is exempted from taxes (E).

On this publish let’s establish the greatest risk-free, most secure and tax-free funding choices. Are there any greatest saving avenues which can be protected, would not have threat related to them and likewise are tax-free, throughout all phases of funding cycle?

Finest Threat-free, Most secure & Tax-free Funding Choices

If now we have to select saving and funding choices which can be completely risk-free, include tax profit and are additionally tax-free on maturity, not many such choices exist.

And the avenues that meet our standards and fall underneath EEE class are as under;

- Public Provident Fund

- Sukanya Samriddhi Scheme

- Worker Provident Fund

- Conventional Life Insurance coverage Insurance policies

Public Provident Fund

PPF is one the preferred saving choices that fall underneath the Exempt-Exempt-Exempt tax classification. This small financial savings scheme is supported by the Central govt and therefore comes with least doable threat. Therefore, it’s the most secure, risk-free and greatest tax-free choice that one can discover.

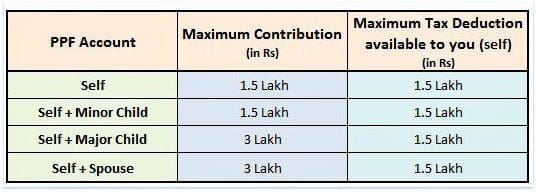

- You possibly can make investments as much as Rs 1.5 lakh each monetary 12 months and might declare earnings tax profit underneath part 80c.

- The curiosity earned on such contributions is tax-exempted.

- The withdrawable quantity on maturity is tax-free i.e., after the 15 12 months lock-in interval ends.

- You possibly can put money into PPF in your identify. You possibly can open just one PPF account in your identify.

- You may also open PPF accounts in identify of your partner or youngsters. Nevertheless, kindly observe that folks (father/mom) can not open two separate PPF accounts within the identify of identical youngster.

- You possibly can make investments a most of Rs.1,50,000 in your identify and minor child’s identify.

- You may also make investments most of Rs 1.5 Lakh in your partner’s identify however do keep in mind you can declare Rs 1.5 Lakh solely as tax deduction.

- For those who put money into identify of your partner, attributable to clubbing of earnings your want so as to add the curiosity earned on partner’s PPF account to your earnings. However observe that PPF account can’t be collectively held.

- You may also put money into your Main youngster’s identify. For instance : You possibly can make investments as much as Rs 3 Lakh in two PPF accounts (self Rs 1.5 Lakh + main youngster PPF A/c Rs 1.5 lakh). You possibly can declare tax deduction of Rs 1.5 Lakh. If the most important youngster has taxable earnings, he/she will be able to deal with the opposite Rs 1.5 lakh as present and might declare tax deduction on his/her earnings.

Sukanya Samriddhi Scheme

Sukanya Samriddhi has related options as that of PPF nevertheless it has barely longer lock-in interval and the contributions might be made within the identify of Lady youngster solely. Like PPF, the Sukanya Samriddhi Scheme additionally fall underneath Exempt->Exempt->Exempt classification. The Sukanya Samriddhi Yojana comes with a sovereign assure (govt. backed small deposit scheme).

- You possibly can make investments as much as Rs 1.5 lakh each monetary 12 months and might declare earnings tax profit underneath part 80c.

- The curiosity earned on such contributions is tax-exempted.

- The withdrawable quantity on maturity is tax-free.

- The contributions need to be made by father or mother / guardian of a lady youngster. Lady youngster is the beneficiary underneath SSA Scheme.

- The contributor (father or mother) can declare the tax deduction on the contributions made to SSA account.

- A depositor can open and function just one account within the identify of identical lady youngster underneath this scheme.

- The depositor (or) guardian can open solely two SSA accounts within the identify of two youngsters.

- SSA might be opened within the identify of a lady youngster from the start of the lady youngster until she attains the age of ten years.

- The scheme would mature on completion of 21 years from the date of opening of the account, with an choice of maintaining the account until marriage. So, the maturity of the account is 21 years from the date of opening of account or if the lady will get married earlier than completion of such 21 years (whichever is earlier).

- The contributions are allowed upto 14 years from SSA account opening date however the SSA financial savings account might be operated until the completion of 21 years from the account opening date.

Associated article : Sukanya Samriddhi Scheme Vs Public Provident Fund (SSA Vs PPF)

Worker Provident Fund

Worker Provident Fund, popularly often called the EPF, is a very talked-about financial savings choice among the many salaried class. The EPF scheme can also be managed by the federal government. Therefore, it affords the best security.

Till the monetary 12 months 2022-23, the EPF was comfortably positioned underneath the tax class of EEE. We are able to nonetheless classify it underneath the EEE regime however with sure circumstances hooked up to it.

- Efficient 1 April 2022, any curiosity on an worker’s contribution to EPF and VPF of upto INR 2.5 lakhs per 12 months is tax-free and any curiosity earned on a contribution over and above INR 2.5 lakhs is taxable within the palms of the workers. (VPF is Voluntary Provident Fund)

- You (worker contributions) can declare tax deduction of as much as Rs 1.5 lakh underneath EPF scheme.

- You possibly can earn curiosity that’s tax-free (supplied you meet the Rs 2.5 lakh threshold restrict). So, in case your contributions ot the EPF scheme is greater than Rs 2.5 lakh in a FY, EPF falls underneath the E-T-E class.

- Your complete EPF steadiness on maturity is a tax-free earnings.

- However kindly observe this level – If an worker who’s a member of EPF scheme, quits or retires from his/her employment and continues holding the amassed PF steadiness, he/she has to pay tax on curiosity from the date of unemployment.

- Additional, from FY 2020-21, if the employer’s contributions to EPF, NPS and the superannuation fund on combination foundation exceed Rs 7.5 lakh in a monetary 12 months, the surplus quantity can be taxable within the palms of the person involved. Any curiosity, dividend, and many others earned on extra contribution will even be Nevertheless, the maturity quantity stays tax exempt.

- Therefore, we are able to say that so long as the worker’s and employer’s contribution threshold limits are usually not breached, the EPF enjoys the EEE tax standing.

Conventional Life Insurance coverage Insurance policies

Ideally, we should always not combine insurance coverage and funding, they need to by no means be mixed. It’s so particularly within the case of conventional life insurance policy, because the anticipated returns on these are abysmally low. (We’re not discussing on ULIPs as their returns are market-linked and include certain quantity of threat.)

However, life insurance policy do fall underneath the class of Exempt, Exempt and Exempt standing however with sure exceptions;

- You possibly can declare a tax deduction of as much as Rs 1.5 lakh u/s 80c on the premiums paid in your life insurance coverage coverage.

- The earnings earned on such plans, just like the survival profit (or) bonuses is a tax-free earnings.

- The coverage maturity quantity can also be tax-exempted, topic to sure circumstances as under;

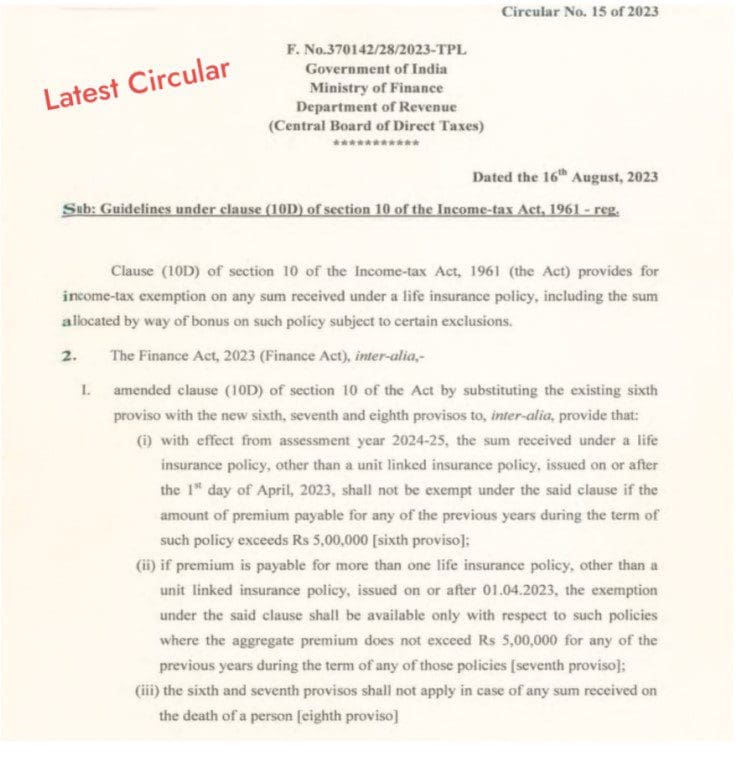

- If the premium paid on life insurance coverage insurance policies, besides ULIPs, exceeds Rs 5 lakh in a monetary 12 months, the maturity proceeds can be taxable. Nevertheless, exemption can be accessible in case of demise of the policyholder. The new taxation regulation will come into impact from April 1, 2023, i.e., FY 2023-24.

- In respect of life insurance coverage insurance policies issued after 1st April 2012, the maturity proceeds obtained are exempt solely and provided that the premium payable in respect of such insurance coverage coverage doesn’t exceed 10% of the sum assured in the course of the premium paying time period.

- In case the premium paid was greater than 10% of the sum assured the distinction between the maturity worth and premium paid solely can be taxable and never the entire of such maturity proceeds

If you’re conscious of the tax implications at varied funding phases, you may be in a greater place to select tax-efficient funding choices. Tax effectivity is a measure of how a lot of an funding’s return is left over after taxes are paid. It’s important to be able to maximize web returns in your investments.

Typically, it’s OK to pay taxes if you can not save or can not put money into proper monetary merchandise. However, don’t make investments simply to save lots of TAXES. The price of shopping for flawed monetary merchandise could outweigh the price of taxes. Tax Planning isn’t a objective however a device. Keep in mind “Tax Planning alone isn’t Monetary Planning.”

Proceed studying:

(Publish first printed on : 30-Aug-2023)