{kind=link}

A reader asks:

Noob query right here…With the potential of rates of interest dropping in a yr or so, ought to a long run investor searching for cheap yields plus capital positive aspects be trying to purchase some bonds proper now? And if that’s the case, what would you have a look at? Thanks!

Not a noob query within the slightest.

Most traders don’t pay a lot consideration to the bond market however I believe bonds have been much more fascinating than shares these previous few years. It’s at all times value revisiting the fundamentals in terms of mounted revenue as a result of bonds will be difficult at occasions.

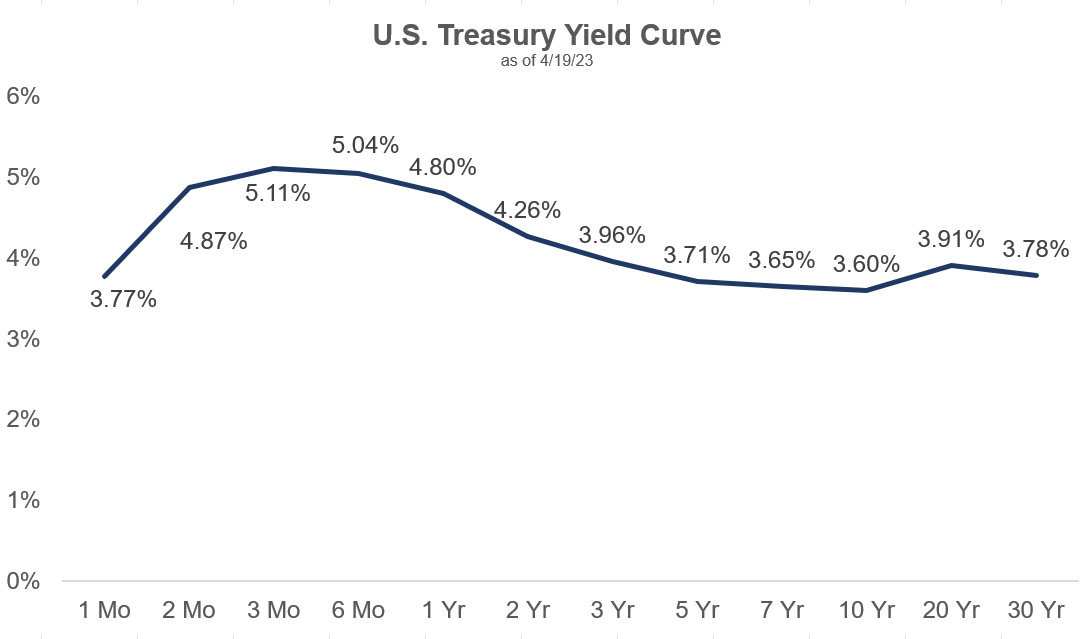

Just a few months in the past I wrote about how T-bills had been the most important no-brainer funding to me with yields of round 5% and the yield curve wanting like this:

Whereas the Fed had compelled revenue traders out on the chance curve because the Nice Monetary Disaster, now traders had been being punished for period threat in a rising fee surroundings. Plus, short-term T-bills had a better yield besides.

T-bills nonetheless look fairly darn engaging, as these yields are nonetheless above 5%. If the Fed raises charges once more, these yields will proceed to go up. However you do face reinvestment threat in T-bills because the period is so quick.

If the Fed retains elevating charges and that throws the financial system right into a recession, they’re going to be compelled to chop rates of interest. Sadly, you possibly can’t lock in these 5% comparatively protected T-bill yields for an prolonged time period.1

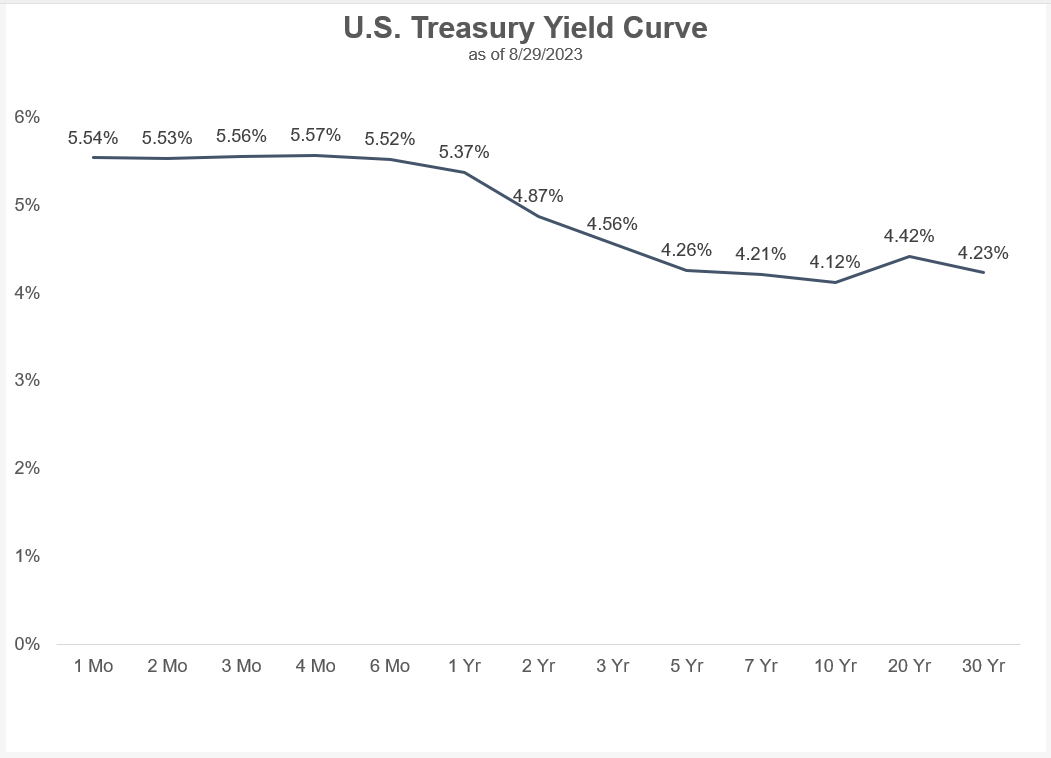

Now check out the up to date yield curve by this week:

The lengthy finish of the curve has caught up a little bit bit. You’ll be able to nonetheless earn a premium in T-bills however the hole has narrowed.

Intermediate-term bonds are wanting extra fascinating from a mix of upper yields and falling inflation.

I’m not a bond dealer however let’s have a look at the case for including some period right here.

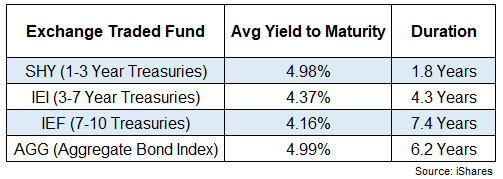

Listed below are the period and common yields to maturity for numerous bond ETFs:

A complete bond index fund (AGG) now yields about the identical as 1-3 yr Treasuries (SHY). That’s nonetheless decrease than T-bill yields however a lot better than the place issues stood only a few quick years in the past.

As a reminder, period is a measure of rate of interest sensitivity on bond costs. A great rule of thumb is each 1% transfer in charges will trigger an inverse transfer in proportion phrases of the period determine.

For instance, IEI has an efficient period of 4.3 years. If charges fell 1%, you’ll anticipate that fund to rise round 4.3%. Conversely, if charges rose 1%, you’ll anticipate the fund to drop 4.3%.

However that’s simply costs.

Now that yields are a little bit greater than 4.3%, you’ll anticipate to interrupt even from that rise in charges in a yr from the yield. In 2020, 2021 and 2022 the beginning yields on bonds had been a lot decrease. You didn’t have that in-built cushion from larger beginning yields.

So whereas bonds may expertise additional draw back threat in costs if charges proceed to go up, there’s now a much bigger margin of security since yields have already risen a lot.

And if charges did rise one other 1%, positive, you’ll expertise some loss in value with a better period however now your beginning yield is 5.3% and also you’re going to make up for these losses a lot sooner.

Beginning yield explains roughly 90-95% of returns for high-quality bonds going out 5-10 years into the long run. So that you don’t actually need yields to fall to earn a good return in bonds.

It is best to really need charges to remain the place they’re or transfer a bit larger from right here so you possibly can lock in larger yields for longer.

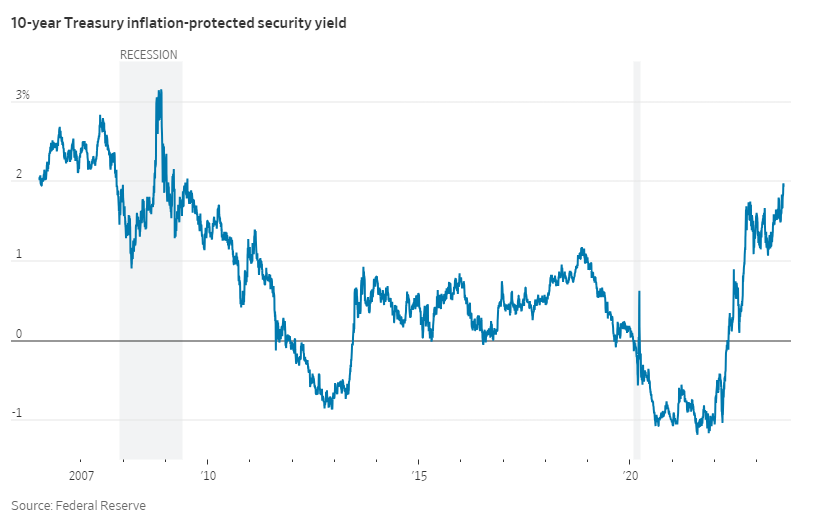

One other constructive growth for bond traders is constructive TIPS yields:

I used to be taught early in my profession that something within the 2-3% vary for yields on Treasury Inflation-Protected Securities is an effective deal. You’ll be able to see on this chart that TIPS yields had been unfavorable for a lot of 2020, 2021 and 2022.

Now you get 2% on 10 yr TIPS plus the inflation kicker. Not a nasty deal.

I don’t faux to have the flexibility to foretell the place rates of interest or inflation go from right here. I choose to have a look at the bond market by way of threat and reward.

I used to be afraid of the bond market in 2020 when charges dropped to their lowest ranges in historical past. The dangers outweighed the rewards by a large margin.2

Now you might have choices galore as a fixed-income investor.

In the event you’re fearful about rising charges or inflation, T-bill yields are the very best we’ve seen in 20 years or so. The Fed is gifting you 5%+ to your protected property.

In the event you’re fearful about deflation, falling rates of interest, a recession or the Fed reducing short-term charges, you possibly can really lock in yields within the 4-5% vary on intermediate-term bonds.

And if you happen to’re fearful about your buying energy, you possibly can earn 2% yields plus inflation on TIPS.

Every of those bond devices has its personal dangers.

For T-bills it’s reinvestment threat. For intermediate-term bonds it’s rising charges and inflation. For TIPS it’s rising charges and deflation.

There are not any free lunches.

It took some ache to get right here however fixed-income traders lastly have some choices after years of paltry bond yields.

We spoke about this query on the most recent version of Ask the Compound:

Jonathan Novy, one in all our advisors and insurance coverage specialists at Ritholtz Wealth, joined me this week to debate questions on emergency funds, investing while you don’t have a 401k, annuity yields and long-term care insurance coverage.

Additional Studying:

Why I’m Extra Anxious Concerning the Bond Market Than the Inventory Market

1The identical is true of CDs. I checked out 5 yr CD yields at Marcus at this time. They’re 3.8%.

2Though I actually did’t foresee a yr like 2022 the place yields would rise as rapidly as they did.