{kind=link}

Earlier this 12 months I continually heard CNBC pundits say, “The Federal Reserve has by no means gotten it proper earlier than, so why ought to we expect they’re proper now?” When discussing the Fed’s fee mountaineering agenda, what I hardly ever heard from the speaking heads on TV had been references to present financial knowledge that actually supported this declare.

As an alternative, they appeared ruled by tales and their feelings.

Close to the tip of September, I wrote about how inflation knowledge supported the Fed’s actions, and why I believed they deserved some reward for navigating us in direction of what more and more seems to be a soft-landing. Nearly seven weeks later the markets lastly appear able to consider it, because of the information in the latest CPI inflation report that was launched Tuesday, 11/14/23.

What was in it that made nearly everybody really feel so good? Let’s take a look at it from the identical perspective I laid out beforehand.

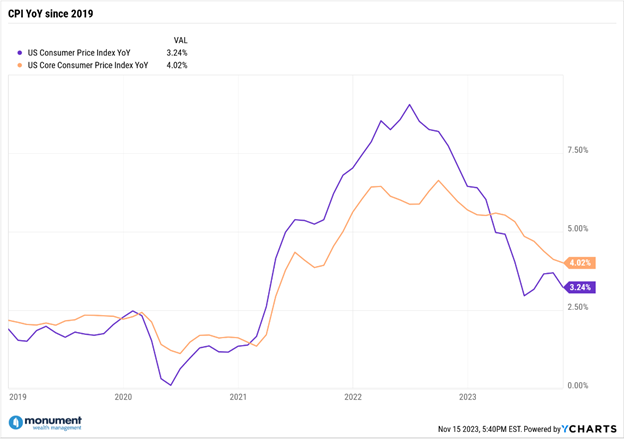

The Distinction Between Headline & Core Inflation

Beginning at a ten,000-foot view: inflation eased in October. Headline year-over-year inflation got here in at 3.24% in the latest CPI report whereas Core CPI inflation registered at 4.02%. As a reminder, Core inflation strips out the sometimes-volatile results of the Meals and Vitality elements. That leaves Housing (the place you reside), Core Items (merchandise you purchase), and Core Companies (stuff you do) as the weather of Core Inflation.

Each the Headline & Core inflation measures in October’s report had been barely under the market’s consensus estimates and under the earlier month’s readings. Decrease than anticipated inflation despatched each inventory & bond costs hovering on the day for the reason that markets interpreted this piece of information as a sign for the tip of fee hikes. Whereas it’s too early to know for positive, I believe they could be onto one thing.

Why? As a result of, as we’ve been saying for some time, the underlying knowledge continues to assist declines in inflation.

We’re Lastly Seeing Declines in Housing Inflation – However Not from Apparent Locations

On this inflationary setting, I’ve targeted on the elements of Core inflation since they’re seen as sticky, or longer-term inflation metrics. Again in August, our co-Founder Dave wrote about how the official knowledge collected for Housing, the most important element of Core CPI, lags what’s really occurring in the true financial system.

It’s taken a while, however we appear to be experiencing a number of the declines in Housing inflation that I’ve written about earlier than. Nonetheless, it isn’t coming from the plain locations. Fortunately, it’s not coming from main declines in residence or lease costs like many anticipated. For my part, a collapse in residence costs or lease ranges may very well be a critically dangerous financial occasion that might be extraordinarily painful for everybody.

As an alternative, the reduction we’re experiencing is because of declines in Lodging Away from Residence, which incorporates lodge and motel charges. In October, Lodging Away from Residence fell -2.5% and has declined in 4 of the previous 5 months.

The Pandemic shut down the globe and created pent-up demand particularly for holidays. It’s no shock that elevated journey demand drove up Lodging Away from Residence costs considerably, which pushed the official Housing inflation knowledge larger. However now we’ve labored off a few of that extra demand and are seeing decrease lodge/motel room costs which are feeding into the official Housing inflation knowledge and are serving to Core CPI proceed to come back down.

The pandemic prompted large imbalances not solely in journey, but additionally within the provide and demand for bodily items, which is one other element of Core CPI. After excessive ranges of Items inflation within the latest years, most of that inflation appears to be behind us with retailers like Walmart’s CEO warning of doable deflation within the coming weeks and months.

These imbalances seem like a major driver of what prompted the spikes in inflation throughout the board. The financial system wants time to rebalance itself, or mentioned in a different way, for the pig to go via the python. As we method the tip of 2023, it’s nice to see a number of the extra demand start to wane, and we’ll hopefully see some stabilization again to pre-pandemic ranges.

You Don’t Want Braveness, You Simply Want Information.

The trail to a soft-landing was affected by landmines and pitfalls. It was by no means a positive factor and wasn’t all the time the consensus. Some may say it took bravery to consider in a soft-landing, however in case you regarded on the underlying knowledge for every of the elements in Core CPI inflation, you didn’t want a lot braveness. Simply perception within the knowledge.

As an investor, in case you can dig a bit deeper into the inflation reviews, you might need seen the soft-landing path that was being specified by the information proper in entrance of you. I’ll say it once more right this moment: The Fed deserves some reward for what they’ve completed up to now, and its thanks partially to their execution of a long-term plan that’s based mostly on precise inflation knowledge.

In all monetary issues, be just like the Fed. Don’t get emotional—take braveness in chilly, laborious, and (generally boring) knowledge. And if the information feels too overwhelming, discover a Wealth Supervisor who might help you make sense of the countless monetary jargon!