{kind=link}

Charitable Reward Annuities (CGAs) have lengthy been a preferred means for people with charitable intentions to plan their legacies. By contributing a lump sum to a charity in alternate for mounted recurring funds for all times (with any leftover funds after the donor’s dying going to the charity), the person can be sure that their funds are directed in the direction of a goal that aligns with their values, whereas additionally retaining a gentle supply of revenue for the remainder of their life. Nevertheless, the caveat with present CGAs has been that they might solely be funded with after-tax {dollars} earlier than the donor’s dying, that means that if a person solely had tax-deferred funds (e.g., in an IRA or 401(okay) plan) to contribute to the Charitable Reward Annuity, they would want to withdraw – and be taxed on – these funds first. Testamentary CGAs, then again, might be established after a donor’s dying, funded with IRA or different property to offer revenue for one more individual. However the SECURE 2.0 Act, handed in December 2022, created the power for people over age 70 1/2 to make a one-time Certified Charitable Distribution (QCD) of as much as $50,000 of IRA funds right into a CGA, with the quantity distributed to the CGA being excludable from the donor’s taxable revenue.

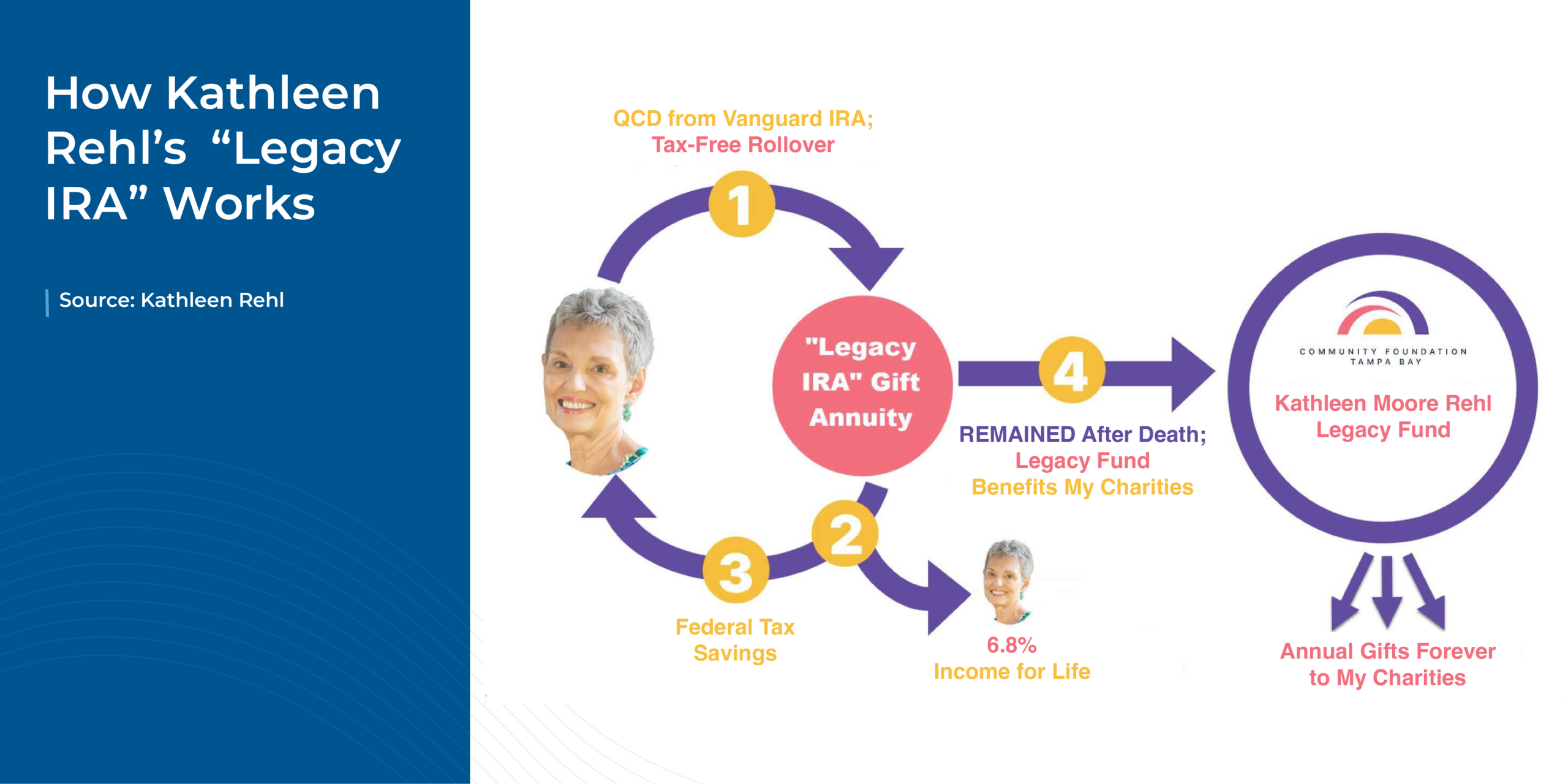

On this visitor publish, Kathleen Rehl, a semi-retired monetary advisor and educator now specializing in her personal property planning issues, shares her expertise with creating her “Legacy IRA” rollover to a Charitable Reward Annuity to help her chosen nonprofits after Congress handed the SECURE 2.0 laws on the finish of 2022.

The potential advantages of the brand new Legacy IRA guidelines are threefold. First, they permit donors to reinforce their charitable giving legacy and guarantee their future charitable intentions are fulfilled. Second, they cut back the donor’s tax invoice within the yr the CGA is created by excluding the quantity contributed to the CGA from taxable revenue. And third, they create a secure lifetime revenue stream that may be paid to the donor and/or their partner.

All of which is necessary throughout a time when members of the Child Boomer era, who’ve collected unprecedented ranges of wealth in comparison with earlier generations, are getting ready to make selections on the way to steadiness their intentions for transferring that wealth – whether or not that be passing it on to the following era of relations or associates, or offering for causes which can be significant to them – with their very own wants for sustainable retirement revenue. And whereas a Legacy IRA could solely be one piece of the puzzle (because the $50,000-per-person lifetime restrict could solely symbolize a small portion of the property of many high-net-worth households), it will possibly nonetheless function a singular and useful legacy and tax planning software – and given the minimal expense and trouble of organising and sustaining the CGA (because the charitable group usually handles all the administrative points of doing so), there could also be no cause for any particular person with charitable intentions and lifelong revenue wants to not use it to the extent that the one-time $50,000 restrict permits!

In the end, for monetary advisors, the Legacy IRA might be one a part of a broader toolkit for serving to retired purchasers with values-based, purposeful legacy planning. By understanding the eligibility necessities and guidelines across the new legislation and reward annuities normally, and having a ‘recipe’ that purchasers can observe for establishing their very own Legacy IRAs, advisors can assist plant the seeds with their purchasers round strategic giving (whereas additionally differentiating themselves to potential new purchasers as a go-to useful resource for property planning and charitable giving)!