{kind=link}

Mortgage Q&A: “Does refinancing damage your credit score rating?”

Everybody appear to be obsessive about their credit score scores and what affect sure actions could have on them.

Maybe the credit score bureaus are in charge, as they’re consistently urging us to verify our scores for any adjustments.

Let’s reduce proper to the chase. On the subject of mortgage refinancing, your credit score rating most likely received’t be negatively impacted until you’re a serial refinancer. Like the rest, moderation is essential right here.

A Mortgage Refinance Will Lead to a Credit score Pull

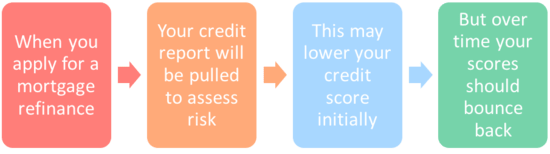

Whenever you refinance your private home mortgage, the financial institution or mortgage lender will pull your credit score report and also you’ll be hit with a tough credit score inquiry because of this.

It’ll keep in your credit score report for 2 years, however solely have an effect on your scores for the primary 12 months.

What’s extra, it should present up on all three credit score reviews with all three credit score bureaus. This consists of Equifax, Experian, and TransUnion.

The credit score inquiry alone would possibly decrease your credit score rating 5-10 factors. However if you happen to’re consistently refinancing and/or making use of for different varieties of new credit score, the inquiries might be much more impactful.

As famous, moderation is the secret right here. In the event that they add up to a degree the place they’re deemed unhealthy, the credit score hit might be bigger.

The credit score rating scientists discovered way back that people who apply for a ton of recent credit score are sometimes extra prone to default on their obligations.

However that doesn’t imply you may’t apply for mortgages and different varieties of credit score if and once you really feel it’s vital.

You May See a Credit score Rating Ding When Refinancing Your Mortgage

- All 3 of your credit score scores could fall quickly because of a mortgage refinance utility

- However the affect is normally fairly minimal, maybe solely 5-10 factors for many shoppers

- And the results are sometimes fleeting, with rating reversals taking place in a month or so

- So it’s sometimes only a short-term credit score hit that received’t have any materials affect

As a result of a mortgage refinance is technically a brand new credit score utility (it’s a brand new mortgage in any case), your credit score rating(s) may see a little bit of a ding.

Nevertheless it most likely received’t be something substantial until you’ve been making use of wherever and in every single place for brand spanking new credit score.

By a “ding,” I imply a drop of 5-10 factors or so. After all, it’s unimaginable to say how a lot your credit score rating will drop, or if it should in any respect, as a result of every credit score profile is totally distinctive.

Merely put, these with deeper credit score histories will likely be much less affected by any credit score hurt associated to the mortgage refinance inquiry, whereas these with restricted credit score historical past could also be see a much bigger affect.

Consider throwing a rock in an ocean vs. a pond, respectively. The ripples will likely be loads larger within the pond.

However in both case, the ripple shouldn’t be a lot of a ripple in any respect, and nowhere near say a late cost as a result of it’s not a unfavourable occasion in and of itself.

It’s extra of a gentle warning to different collectors that you just’re presently looking for new credit score.

[What credit score is needed to buy a house?]

You Get a Particular Buying Interval for Mortgages

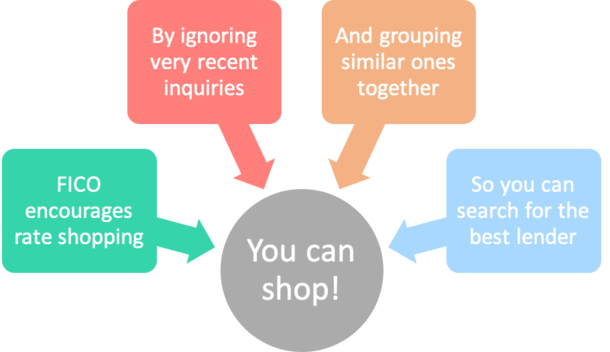

- FICO ignores mortgage-related inquiries made within the 30 days previous to scoring

- And treats comparable inquiries made in a brief interval (14-45 day window) as a single laborious inquiry

- As an alternative of counting a number of inquiries in opposition to you for a similar mortgage

- This may occasionally enable you to keep away from any unfavourable credit score affect associated to your mortgage search

First off, notice that on the subject of FICO scores, mortgage-related inquiries lower than 30 days previous received’t rely in opposition to you.

And for mortgage inquiries older than 30 days, they could be handled as a single inquiry if a number of ones happen in a small window.

For instance, searching for a refinance in a brief time period (say a month) could lead to a lot of credit score pulls from completely different lenders (if you happen to store round).

However they may solely rely as one credit score hit as a result of the credit score bureaus know the routine on the subject of searching for a mortgage.

They usually really need to promote purchasing round, versus scaring debtors out of it.

In any case, if you happen to’re solely trying to apply for one dwelling mortgage, it shouldn’t rely in opposition to you a number of occasions, even when your credit score report is pulled with a number of lenders.

It’s Completely different for Different Sorts of Credit score

This differs from searching for a number of, completely different bank cards in a brief time period. This might damage your credit score rating(s) extra since you’re making use of for various merchandise with completely different card issuers.

So somebody going nuts attempting to open three bank cards within the span of a month may see their scores tank (I’m you bank card churners).

Even if you happen to store for a mortgage refinance with completely different lenders, if it’s for the identical single objective, you shouldn’t be hit greater than as soon as.

Nonetheless, notice that this purchasing interval could also be as brief as 14 days for older variations of FICO and so long as 45 days for newer variations.

For those who area out your refinance purposes an excessive amount of you may get dinged twice. Even so, it shouldn’t be too damaging, and positively not sufficient to forestall you from purchasing completely different lenders.

The potential financial savings from a decrease mortgage fee ought to positively trump any minor credit score rating affect, which as famous, is short-lived.

The mortgage, however, may stick with you for the following 30 years!

You Lose the Credit score Historical past As soon as the Previous Mortgage Is Paid Off

- Whenever you refinance your mortgage it pays off the previous mortgage

- That account will finally fall off your credit score report (in 10 years)

- And closed accounts are much less useful than energetic ones

- However the brand new account ought to make up for the misplaced historical past on the previous account

One other potential unfavourable to refinancing is you lose the credit score historical past advantage of the previous mortgage account, as it might be paid off through the brand new refinance.

So in case your prior mortgage had been with you for say 10 years or extra, that account would change into inactive when you refinanced, which may price you just a few factors within the credit score division as properly.

Keep in mind, older, extra established tradelines are your credit score rating’s finest asset. So wiping all of them out by changing them with new traces of credit score may do you hurt within the short-term.

Moreover, it may have an effect on the common age of all of your credit score accounts (credit score age), which can also be seen as a unfavourable.

However the financial savings related to the refi ought to outweigh any potential credit score rating ding, and so long as you apply wholesome credit score habits, any unfavourable impact must be minimal.

[Does having a mortgage help your credit score?]

Money Out Refinance Means Extra Debt, Probably a Decrease Credit score Rating

- A money out refinance may damage your credit score scores much more

- Because you’re taking out a brand new, larger mortgage within the course of

- Bigger quantities of debt and better month-to-month funds naturally enhance default danger

- So it’s doable your credit score scores could also be impacted extra if you happen to faucet your fairness

Additionally contemplate the affect of a refinance that ends in a bigger mortgage steadiness, reminiscent of a cash-out refinance.

For instance, in case your present mortgage steadiness is $350,000, and you’re taking out an extra $50,000, you’ve now obtained $400,000 in excellent debt.

The bigger mortgage steadiness will enhance your credit score utilization, and it may lead to a better month-to-month cost, each of which may push your credit score rating decrease.

In brief, the extra credit score you’ve obtained excellent, the better danger you current to collectors, even if you happen to by no means really miss a month-to-month cost.

Refinance Financial savings Ought to Impression Credit score Rating Ding

In abstract, a refinance ought to have a compelling sufficient purpose behind it to eclipse any credit score rating issues.

Deal with why you’re refinancing your mortgage first earlier than worrying about your credit score rating.

In the end, I’d put it on the no-worry shelf as a result of chances are high the refinance received’t decrease your credit score rating a lot, if in any respect. And rating drops associated to new credit score sometimes reverse in a short time.

So even when your credit score rating fell 20 factors post-refi, it might most likely achieve these factors again inside just a few months so long as you made on-time funds on the brand new mortgage.

And most of the people are solely involved about their credit score scores proper earlier than making use of for a mortgage, so what occurs shortly after your private home mortgage funds could not matter a lot to you.

However to make sure you don’t get denied on account of a credit score rating drop, it’s useful to have a buffer, reminiscent of an 800 credit score rating in case your rating does drop a bit whereas purchasing round.

For those who’re proper on the cusp of a credit score scoring threshold and your rating dips barely, you may wind up with a better curiosity, or at worst, be denied a mortgage outright.

Learn extra: When to refinance a house mortgage.